Why is the balance sheet a key to understanding a company?

Public companies report financial statements every quarter to provide helpful accounting information for investment decisions. The balance sheet (also called the statement of financial position or statement of financial condition) is one of the three significant financial statements. It discloses what an entity owns or controls (assets), what it owes (liabilities), and what the owners' claims (equity) are at a specific point in time.

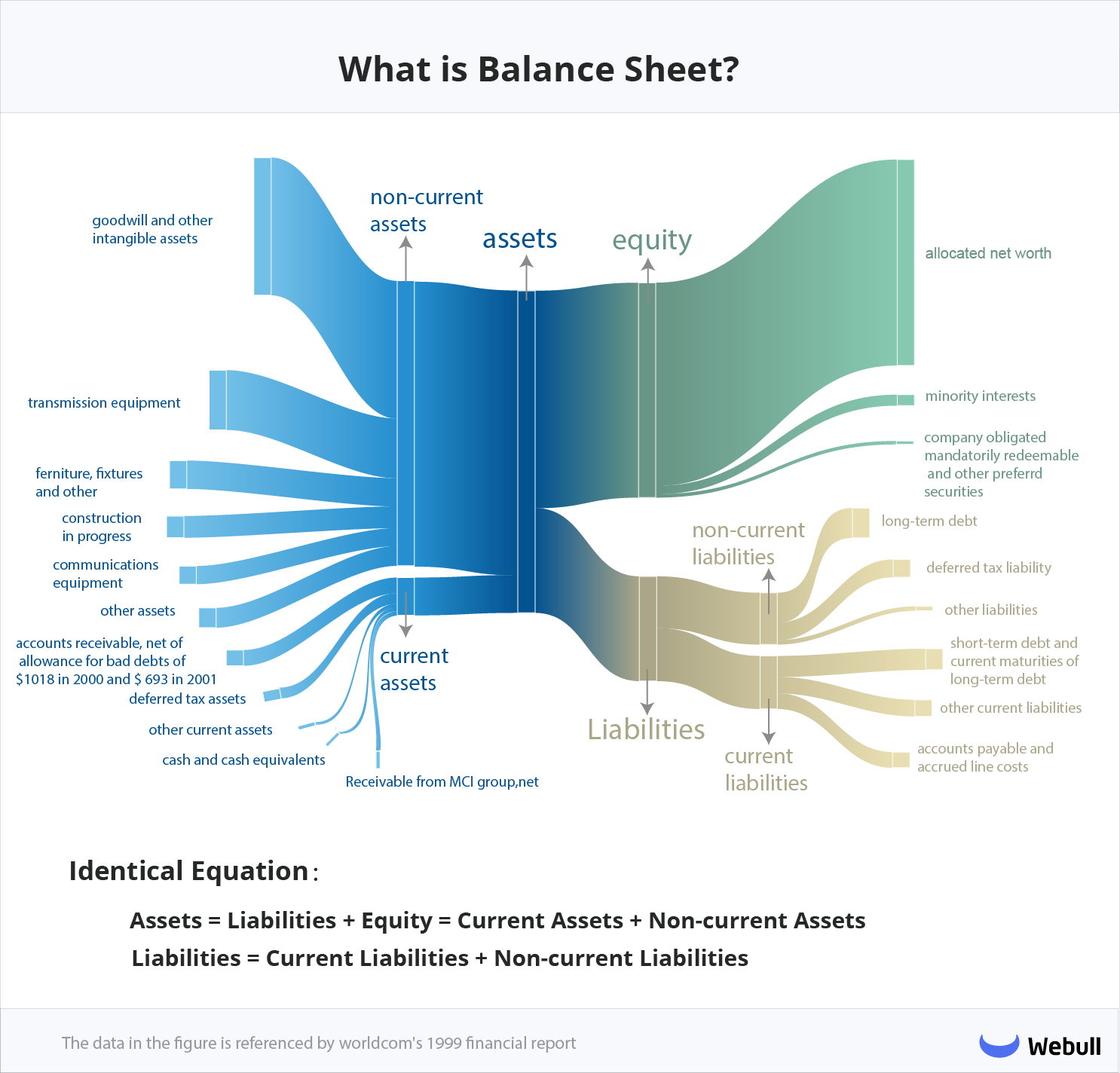

There is an identical equation among these three. We made an infographic to introduce the component of the balance sheet.

Here is a detailed explanation of the critical elements of the balance sheet.

Assets are what the company owns.

Assets(A) is what the company owns (or controls). More formally, assets are resources controlled by the company based on past events. Additionally, future economic benefits are expected to develop for the company’s gain, and are crucial to an asset’s success. An asset is something that, in the future, can generate cash flow, reduce expenses, or improve sales, regardless of whether it's manufacturing equipment or a patent.

Assets can be divided into two categories: current assets and non-current assets. Current assets are generally cash or otherwise realized in cash within one year or one business's operating cycle. Non-current assets are usually long-term, long-lived assets, something expected to be sold or used up within one year or one business's operating cycle.

Liabilities are what the company owes.

Liabilities(L) are what the company owes, usually a sum of money. More officially, liabilities mean obligations of a company derived from past events. The resolution expects an outflow of economic benefits as a result of these events. Just like assets, liabilities consist of current and non-current liabilities. The separate presentation of current and non-current assets and liabilities enables an analyst to examine a company's liquidity position (at least as of the end of the fiscal period). Current liabilities are usually considered short-term (estimated in 12 months or less), while non-current liabilities are long-term (12 months or greater).

Equity represents the shareholders' stake in the company.

Equity(E) represents the owners' residual interest in its assets after deducting its liabilities. Unlike assets and liabilities, equity cannot be split between current and non-current, commonly known as shareholders' equity or owners' equity. It is determined by subtracting the liabilities from the assets of a company, giving rise to the accounting equation: A – L = E or A = L + E.